What can be done to maximize your operations strategy.

In the mid-1700s, Alexander Webster and Robert Wallace, two ministers of the Church of Scotland caused a major change that would alter the life insurance landscape forever. The plan they devised would invest the revenue from policy premiums and use the income generated from those investments to payout death benefit claims to the families of the insured. Much of the success of the newly-created fund can be credited to Wallace and Webster’s precise use of actuarial science such as understanding mortality rates of Scottish clergymen, along with life expectancies of the ministers’ wife and children.

A novel concept then, quite the norm now. Because of the two minister’s research and their understanding of actuarial concepts they created the template for the modern life insurance company.

Fast forward 250 years, and you’ll find an insurance industry that has experienced numerous regulatory changes and a wave of mergers & acquisitions (M&A) that leaves it consolidated and massively restricted.

Between 1993 and 2009 there have been 102 M&A transactions conducted by the largest listed European insurance acquirers totaling an absolute transaction value of €245 billion. - University of Köln, Research Paper

The last years, however, the focus has been on Technology and Customers; the pace of technological change continues to accelerate, and customer expectations are growing. If the shake-out in other commercial sectors teaches us anything, it is that no business, including Insurers, is immune from today’s rapid shifts in technology capabilities and customer expectations, which drives a demand for greater customer service and forces entire industries to digitally transform.

Reducing operating costs

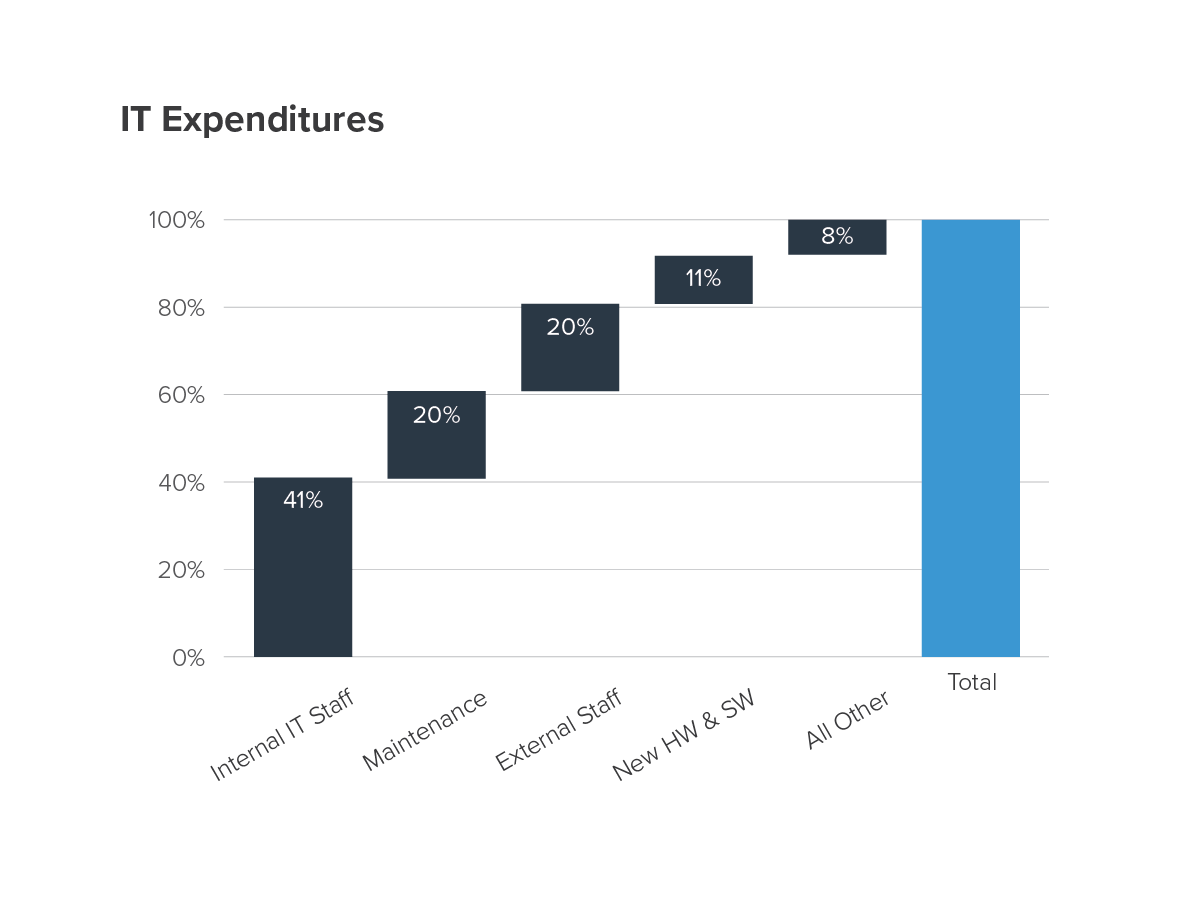

IT spending as a percentage of direct written premium for Insurers has been hovering between 3.5% and 3.8% the past 5 years. Within that IT spending, on average, the Insurance industry spends 66% on ‘running the business’, 27% on ‘growing the business’ and only 12% on ‘transforming the business’. The lack of funding for digital transformation is similar to the banking industry.

All the M&A activity has resulted into a proliferation of policy administration systems and other applications to manage the business. This is probably one reason why the average IT FTEs expenditures in Insurance is more than 60% (Internal 41% and External Staff & Services 20%) of the total IT budget.

Considering these statistics, the cost to manage a policy is high compared to digital challengers. Insurers are looking at reducing operating costs focused on sunsetting admin platforms and removing dependencies on expensive to maintain applications.

While Insurers are focusing more on the customer, they are increasingly prepared to have the business process services (BPS) run by a 3rd party administrator (TPA). Basically, the policies are converted to a single (cloud) platform and employees of the TPA execute claims processing. Here are some examples that demonstrate the significance of BPS:

- CSC to Manage Closed Block Retail Life and Annuities for MetLife (Link)

- Scottish Widows partners with Diligenta to enhance its service for heritage customers (Link)

- WNS, Genpact bag $300-m contract from Australian Suncorp (Link)

Not all Insurers are moving along this TPA path. The cost of migration to an outsourcer’s systems can be prohibitively high. There are also costs associated with integrating the outsourcer’s platform with the internal systems such as finance, commissions, valuation, risk and reporting. If a conversion fails, or is delayed, it can not only erode the savings expected, it can also result in a degradation in customer service causing noise in the marketplace.

There are deals to be done

If the decision is made to go down the path of BPS, the only option the Insurer has is to run a rigorous BPS selection process and a comprehensive transition project using the right advisors to minimize the risk and maximize the value.

It is NET(net)’s view that TCS – through Diligenta and the BaNCS system – is the market leader. They have entered into large and highly visible agreements recently. The downside is that this has stretched their ability to deliver, with Insurers asking: Are we getting their A-Team? Competitors such as HCL, Wipro, WNS, Accenture, Majesco, Genpact and ATOS continue to be aggressive, and are more than willing and capable to step into this void as the Insurance BPS market continues to grow.

So, what does this mean if you are considering BPS:

- Locate Software Contracts – Some agreements may be decades old or negotiated by a business owner who left the company. If these deals are not in your Contract Management System make sure you allow time to collect this information.

- Review Software Contracts – Reviewing these agreements to determine if you have Third Party Use or License Transfer Rights and what Termination for Convenience language is included is a tedious task but necessary to determine exposure. Although the amount of money needed to secure these rights may be negligible compared to the overall deal, it is a negotiation that can be used to maximize your overall value.

- Determine Infrastructure Impact – Reducing compute needs in the Data Center because of BPS has many implications including an impact on cost allocation of remaining volumes. That is an opportunity to renegotiate (hardware and software) contracts, transition applications to the cloud and introduce competitive challengers.

- Develop Skills Matrix – The retained Supplier Management organization requires a redesign to ensure that managing the BPS outsourcer becomes a key competency. A review of the Supplier Risk Management function to ensure appropriate focus on Quality Assurance (for example: Are Supplier Audits performed?) and Quality Control (for example: During the Supplier Audit were the right questions asked?) is also required. For European Insurers, complying to GDPR as a Data Owner and working with a Data Processor becomes more than relevant.

Call NET(net)

Wallace and Webster were transformational centuries ago. Insurers today are facing another seismic shift in how the business is run. We can help with every step listed above and have a complete program that can help disentangle contracts, optimize value of IT investments and mitigate supplier management risks.

- Agreement: Terms, Conditions, Remedies, Negotiation or Renegotiation

- Investments: Associated Risk, Cost out for transformation/shift of assets

- Relationships: Metrics to manage, sourcing of new or alternative suppliers

To schedule a discussion on our Advisory, Sourcing and Optimization services specific to our Insurance Practice or any Technology Supply Chain questions, contact Dexter Siglin at dsiglin@netnetweb.com, and we’ll arrange for a Subject Matter expert to review your situation.

About NET(net)

Celebrating 15 years, NET(net) is the world’s leading IT Investment Optimization firm, helping clients find, get and keep more economic and strategic value. With over 2,500 clients around the world in nearly all industries and geographies, and with the experience of over 25,000 field engagements with over 250 technology suppliers in XaaS, Cloud, Hardware, Software, Services, Healthcare, Outsourcing, Infrastructure, Telecommunications, and other areas of IT spend, resulting in incremental client captured value in excess of $250 billion since 2002. NET(net) has the expertise you need, the experience you want, and the performance you demand. Contact us today at info@netnetweb.com, visit us online at www.netnetweb.com, or call us at +1-866-2-NET-net to see if we can help you capture more value in your IT investments, agreements, and relationships.

NET(net)’s Website/Blogs/Articles and other content is subject to NET(net)’s legal terms offered for general information purposes only, and while NET(net) may offer views and opinions regarding the subject matter, such views and opinions are not intended to malign or disparage any other company or other individual or group.